In October the S&P coughed up over 7% and the technology sector sold off nearly 8.5%. Volatility spiked and general investor sentiment turned sour over the course of the month, albeit minor gains followed from midterm elections early this week. Could we be near the end of the longest bull run in American history?

Obviously nobody knows, but I will attempt to outline the reasons for which the recent pullback could be the beginning of the end, and why it may just be a blip in the radar.

For those of you getting nervous, you’re likely considering where we stand from a valuation perspective. Equities multiples are high but not grotesquely overvalued (S&P stands just above 18), and this will draw the attention of a value investor. That said, we have seen the markets maintain high PE ratios for extended periods of time, thus this is merely one piece of the puzzle to consider. Relatively high valuations just mean you must be very careful about the battles you pick.

Then there’s housing volume. In October, U.S. existing home sales dipped below 2013 levels, and are down ~9% YoY. Although financial products in this space are subject to greatly increased regulation given a ~couple things~ that transpired a decade ago, weakness in the housing market has been known to unsettle investors, justifiably so.

As is timely considering midterm elections, market skeptics will also consider the political landscape. There has existed an interesting trend regarding presidential terms and market performance: Broadly, during the first two years of Republican presidencies, the markets have outperformed, then underperformed the second two years (and vice versa for Democrats). We now approach the second half of the Trump presidency with a divided Congress. Policymaking proved an arduous process during the first two years under a unified Congress and Oval Office; I expect a split Congress to further challenge the President in his goal to advance his agenda under more adverse political conditions.

For those who think the markets may continue in their impressive run, there are also a number of healthy signs to consider:

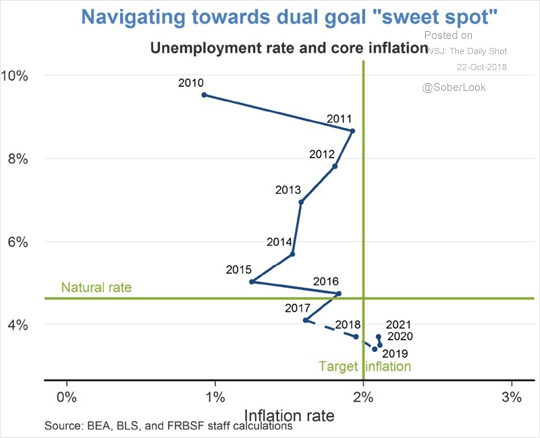

Employment is strong, and is approaching a healthy balance with inflation (see chart).

I like this chart because it aptly depicts the hypothetically ideal equilibrium of inflation at 2% and unemployment just shy of 5%, while including projections for how that balance may evolve considering future FED rate hikes (this week the FED held rates constant). Presently, the U.S. stands below the ideal point of unemployment, and the FED has responded with rate increases in an attempt to migrate towards equilibrium, even though inflation remains low. Expect the FED to continue in its goal of shrinking its balance sheet, the consequences of which include investors who are afraid that there is no longer “easy” access to capital, thus the markets may pull back temporarily with each respective rate increase.

While equity valuation may be on the high side, tax cuts have provided firms with the opportunity to invest in R&D, execute long awaited share buybacks and increase dividend payouts. This should help in driving future value for shareholders, regardless of the valuation landscape. If you just consider the fraction of stock Price divided by Earnings per share, hopefully tax cuts lead to firms bolstering the denominator for continued returns.

Additional positives include the fact that America’s dependence on foreign oil is not as great as it once was considering high levels of U.S. production. This also reduces the consequences of tensions with the Middle East; if conflict abroad intensifies, expect oil to skyrocket less than it might otherwise. This has positive implications for consumer goods as well; prices increase when transportation costs likewise spike. Not to mention oil has officially entered bear market territory this week.

There are numerous other factors at play bolstering both sides of the argument, but these are the macroeconomic developments I view most relevant when contemplating the possibility of a recession in the next couple years. Should one of these factors take a turn up or down, expect there to be effects in the markets.

Referenced material:

Cartoon: Bush and the Snake, Olle Johansson